Submission to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry

The Prudential Inquiry into the Commonwealth Bank of Australia (CBA) Final Report, May 2018, said:

CBA’s continued financial success dulled the senses of the institution… In the environment of continued financial success, two critical voices became harder to hear… One was the ‘voice of risk’

I would not seek, in any way, to diminish this statement in reference to the Commonwealth Bank of Australia.

However, the real question is whether this attitude has a far wider relevance in the Australian community than this one institution, and perhaps a few others that have been revealed thus far in the Royal Commission.

My understanding is that this Royal Commission is the first into the banking and financial services industry in around 70 years, and, given the twists and turns that took place for it to come into existence, it is clear to all Australians that this is going to be our one and only chance to get to the bottom of this question.

Therefore, I wish to add my voice to that of others who have stated the need to extend the duration of the inquiry and to increase it’s Terms of Reference (TOR).

I understand that regulation was expressly excluded from the TOR. I believe that this must be reversed. Already during the Commission proceedings there have been many questions raised about the role that regulators have played in below acceptable standards becoming entrenched within the industry.

It is clear that if we genuinely want effective regulation by the Australian Prudential Regulation Authority (APRA) and the Australian Securities and Investment Commission (ASIC), then we need a much deeper dive into how these organisations interact with the private sector; what disadvantages they face in that interaction; and any potential conflicts of the organisation and/or individuals.

Our financial services industry has a major focus on residential housing with around 60% of our banks’ assets consisting of residential mortgages, a far greater proportion than in any other similar country or economy.

At times over the last decade and a half it has seemed that managing the risks surrounding the housing market has been the most critical financial issue confronting the country, and consequently this demands significantly more attention from the Commission than can occur within the current time frame and TOR.

Herein I wish to draw particular attention to apparently inconsistent framing of issues by APRA, ASIC, and especially the other regulatory member of the Council of Financial Regulators, the Reserve Bank of Australia (RBA).

At ASIC’s annual forum in early 2017 our housing market had returned to being such a vulnerability to our economy that the heads of two of our regulators – APRA and ASIC – normally staid, conservative, and austere commentators of our economy – spoke about the extreme build-up of risks in our housing markets in Sydney and Melbourne in graphic terms alerting all to their strong concerns.

In fact, Mr. Medcraft (ASIC) described these markets as being in a price bubble! For the head of a federal regulator to say that is truly remarkable!

My reading of the situation is that the only reason Mr. Byres (APRA) stopped short of joining him is because he “does not use the B-word”!

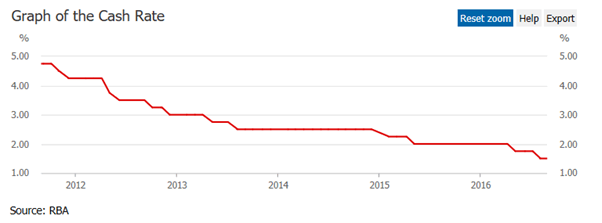

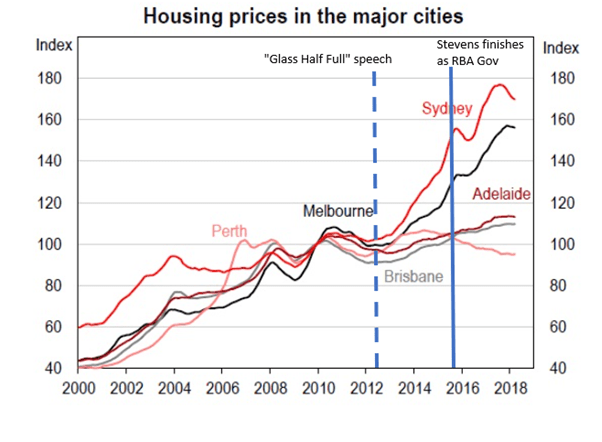

To understand this remarkable turn of events it is instructive to turn the clock back less than 5 years to two speeches delivered in mid-2012 by the then RBA Governor, Glenn Stevens. To fully capture the essence and gravity of the disparity, I present Exhibit 1 – RBA policy rates over the period, Exhibit 2 – house price movements in our major cities, and then below are extensive quotes from these two speeches (the emphases are my own, together with some italicised comments).

Exhibit 1. RBA cash rate policy from 2011 to late 2016.

Exhibit 2. Australian house prices highlighting period between June 2012 and September 2016 (when Glenn Stevens finished as RBA Governor)

“The Glass Half Full”, Glenn Stevens, Governor of RBA, address to the American Chamber of Commerce (SA) AMCHAM Internode Business Lunch Adelaide, 8 June 2012

I think this is a profoundly important point and worth emphasising. The decade or more up to about 2007 was unusual. It would be quite surprising, really, if the same trends – persistent strong increases in asset values, very strong growth in per capita consumption, increasing leverage, little or no saving from current income – were to re-emerge any time soon.

That the only aspect of this trend that has not re-emerged is the very strong growth in per capita consumption – in large part due to historically low wages growth – only worsens the comparison.

In fact, without the mining boom and its spillovers, we would have been feeling the effects of those adjustments rather more acutely than we do now. The period of household gearing up could have ended in a much less benign way.

Now that the build out of extra mining capacity is largely completed, the spillovers are much reduced across our economy, emphasising the greater risk that Australian households now face.

One thing we should not do, in my judgement, is try to engineer a return to the boom. Many people say that we need more ‘confidence’ in the economy among both households and businesses. We do, but it has to be the right sort of confidence. The kind of confidence based on nothing more than expectations of ever-increasing housing prices, with the associated willingness to continue increasing leverage, on the assumption that this is a sure way to wealth, would not be the right kind. Unfortunately, we have been rather too prone to that misplaced optimism on occasion. You don’t have to be a believer in bubbles to think that a return to sizeable price increases and higher household gearing from still reasonably high current levels (Stevens’ emphasis) would be a risky approach. It would surely be a false basis for confidence. The intended effect of recent policy actions is certainly not to pump up speculative demand for assets.6 As it happens, our judgement is that the risk of reigniting a boom in borrowing and prices is not very high, and this was a key consideration in decisions to lower interest rates over the past eight months.

Clearly, with the benefit of hindsight, history does not reflect kindly on the entirety of this paragraph because Glenn Stevens’ and the RBA board’s judgement has proven demonstrably very incorrect.

The frequent mention of the word “confidence” shows the RBA perceives the fostering of this to be a major aspect of it’s role in the economy, and that it considers itself under some pressure from some unnamed quarters to “provide it”.

Moreover, it is clear that the RBA board understood just how prone our society has been to not hearing the “voice of risk” surrounding leverage and our housing market.

What’s more, the poor judgement by the RBA, and perhaps other financial regulators, to reduce interest rates but be reluctant (and in Glenn Stevens respect, to be openly sceptical) to introduce more timely macroprudential tools – suggests that the earlier success at managing through the Global Financial Crisis dulled the regulators’ senses so that the “voice of risk”, which, while recorded, was not given the gravitas that was required.

And to repeat, it is not our intention either to engineer a return to a housing price boom, or to overturn the current prudent habits of households.

But that is exactly what occurred! No sooner did the Governor utter these words did households recommence their former imprudent habits, and the regulators have since been continually behind the curve culminating in an almost panicked response from regulators in early 2017 suggesting the “voice of risk” suddenly found a megaphone!

“The Lucky Country”, Glenn Stevens, RBA Governor, address to The Anika Foundation, 24 July 2012

It has long been a visceral fear among Australian officials and economists that global investors will suddenly take a dim view of us. The same sorts of concerns of organisations such as the International Monetary Fund and the ratings agencies seem to lie behind a perpetual question mark about Australia and its financial institutions.

In this speech Governor Stevens reiterated many of the themes touched on in the speech delivered 7 weeks earlier and begins to expand on where much of the actual risk lies. Importantly, these concerns then were already held by international organisations such as the IMF and ratings agencies.

You don’t suddenly acquire the credibility needed to ease monetary policy aggressively while the exchange rate is heading down rapidly.

By extension, that credibility is not likely easily maintained, either, and other comments by Glenn Stevens in the post-GFC period highlighted how that credibility could be quickly lost in periods of stress.

We should never say a crash couldn’t happen here, and the Reserve Bank continues to monitor property markets and the performance of mortgages quite closely, as we have for many years. But it has to be said that the housing market bubble, if that’s what it is, seems to be taking quite a long time to pop – if that’s what it is going to do. The ingredients we would look for as signalling an imminent crash seem, if anything, less in evidence now than five years ago.

Even though the Governor says the RBA is alert to the risks surrounding a housing bubble, this statement is in fact suggestive of a degree of hubris and dulling of senses. What’s more, within 5 years of making this statement risks were clearly at or above that previous period.

Housing values and leverage in Australia couldn’t keep rising. They haven’t.

The Governor said they couldn’t keep rising – but they recommenced their rise after only a very brief interruption around the time that these two speeches were made. And now we need to deal with the consequence of something that couldn’t happen – because, by inference, the risks were too great to contemplate – that did in fact happen!

These events, together with what had occurred in Australia over the previous decade, suggest that there may be a policy asymmetry amongst our regulators which needs to be very closely examined.

Moreover, not all financial policy is entirely transparent, especially to a public which is frequently stated to be less financially/economically literate than the bureaucratic and financial sector apparently would want it to be.

(This is the public that foots the bill for those policy measures.)

As just one example, on the “Ticky” programme on Sky News Business in May 2018, Brian Jonson of CLSA (frequently referred to as the top analyst for Australia’s finance sector) said the following (and I paraphrase because I have been unable to find a transcript or footage of the exchange – in fact I was unable to locate online any reference to the changes to which he refers):

“Analysts seems to misunderstand what an enormous gift the RBA has given to the banks where the committed liquidity facility was expanded in the budget to $248 billion!”

Clearly, if professional finance analysts do not understand it, either because of complexity or a degree of information obscurity or opaqueness, one has to question whether there really is desire among the political/bureaucratic/private-sector complex for greater financial literacy and understanding of the breadth of policy issues affecting housing and broader financial markets.

The Nexus Between the Political, Regulatory and Private Sector Financial Communities

(For the purposes of this submission I will leave aside the other sector of society which clearly plays a role here – the media.)

John Howard famously said in 2003 during a radio interview that nobody ever complained to him about the price of their home going up.

I am a homeowner. My wife and I managed to buy a few years back after it looked for a while that a commitment to contributing to society through a career in scientific research may have cost us the opportunity to ever own a home in the city where we settled.

However, a few weeks back I had a thought which led to an overwhelmingly depressing feeling inside of me. The thought was this:

“What if prices remain at these high levels (relative to income) for the next couple of decades so that my children will be faced with deciding between never owning a home or committing significantly more of their lifetime incomes towards paying off a home, and living under the significant stress of knowing that they are considerably more vulnerable should interest rates rise, than previous generations of Australian?”

By now I am somewhat of a veteran in putting forward a view that high house prices are not advantageous for our country and our society, and that it would be better for our society and especially our future generations if homes were once again priced according to their value in providing shelter rather than as speculative assets.

In 2008 I started a website named “homes4aussies” and over the years I have participated in numerous Government financial inquiries and other political processes. There are a few anecdotes that I could share, such as my experience at my local 2020 summit in Griffith (the electorate of the then Prime Minister, Kevin Rudd.) However, the experience I think is most pertinent here is what occurred at a community cabinet meeting in northern Brisbane in March 2008.

I learned of the meeting only a few days in advance but managed to get approval to attend. I asked a question from the floor which essentially sort from Prime Minister Rudd a confirmation that his recently elected Government genuinely wanted to return the “fair go” to the housing market so that all Australians could have confidence that they would had a realistic chance at attaining the Australian dream of home ownership. (see “Rudd grilled on housing, health”, https://www.smh.com.au/national/rudd-grilled-on-housing-health-20080302-1wa1.html)

My question received applause from the audience. However, the tone of Prime Minister Rudd’s response was one of annoyance and was an early indication to me of his now infamous temper.

More pertinent, however, was what occurred as the open forum part of proceedings finished and I approached the then Treasurer, Wayne Swann, to enquire whether it might be possible to meet privately to discuss the issues surrounding housing affordability.

From arm’s length he looked me in the eyes and smugly said that I was dreaming if I thought that negative-gearing would ever be ended!

In my question from the floor I had highlighted that I was a retired scientist – that I had been a part of the “brain drain” (even named in Government reports in my field) – and that the dream of home ownership was a part of my reasons for me quitting and becoming a stay at home dad while my accountant wife, with significantly higher earning potential, became the “bread winner” (as I also outlined to the Senate Select Committee on Housing Affordability hearings in Brisbane). I also outlined how in the few short years I worked overseas as a scientist house prices in Brisbane doubled, and had gone on to triple by 2008.

What I did not say, in either forum, but am prepared now to say publicly – since it is unlikely I will ever work again – is that I had a breakdown when I quit my career, 3.5 years earlier.

I also highlighted in the open forum how our rent had been increased by 20% – or $260 per month – just a couple of months earlier. (Our rent was increased again 6 months later for an annual increase of over 30%!)

With one child and another on the way we were finding saving for a prudent-sized home deposit challenging, and the dream of home ownership seemed to be sliding further and further away from us.

To say that I was fragile and vulnerable at the time would be a significant understatement. And to be taunted at such close quarters by such a powerful and influential man – no less than the Treasurer of the country! – well I am not ashamed to say that it took every ounce of strength that I could muster to maintain control and hold myself back from landing a blow on his jaw! (Having been a representative front-rower in my younger years, as a young man from the country I was not averse to sorting things out “the old-fashioned way”.)

I felt like I was shaking, and I remain in no doubt that the people surrounding Mr. Swann – some presumably security personal – were on high alert.

Of course, my recovery is far more progressed, and I am now far less vulnerable than I was at that time, but I still reflect on just how smug, arrogant, egotistical and heart-less Mr Swann’s actions were on that day.

I suggest that, together with the views expressed by John Howard, and occasional quips by senior economic bureaucrats (such as the one by Glenn Stevens’ that in his experience people tend to change their views on what is desirable for house price movements after they buy), show conclusively that there is un upward bias to housing markets amongst the powerful politico-bureaucratic complex in Australia.

If one is inclined to agree with Glenn Stevens’ view of a conscious or sub-conscious bias relating to one’s home- or property-owning status, then by extension it can only be interpreted as an admission that the individuals having the most influence over housing policy are indeed biased towards higher house prices. For example, research shows that politicians, as a group, are very significantly over-represented in society as property owners – Federal Parliament members and senators are twice as likely as the general populace to own their own home, and they are almost 5 times more likely to own investment property. (see http://www.abc.net.au/news/2017-04-20/housing-affordability-decisions-made-by-big-property-investors/8454978)

Moreover, recent appointments in the private sector in the financial services industry suggest that biases – either conscious or sub-conscious – extend beyond the propensity for the political and senior bureaucratic community to be active in housing markets.

In recent years, two former State Government Premiers have taken senior roles in the financial services industry – Anna Bligh as CEO of the Australian Banker’s Association and Mike Baird as a senior executive in NAB (note that the NAB CEO even admitted to the Sydney Morning Herald that he discussed employment opportunities with Mr Baird while he was still Premier), the former New Zealand Prime Minister has taken a senior role in the ANZ bank, the former Treasury Secretary Ken Henry has taken a role as Chairman of NAB, and Glenn Stevens has been appointed an independent director of Macquarie Bank.

Given the facts presented above, the appearance surrounding

such appointments does not pass the “pub test” (the political buzz word of the

moment) in my opinion.

Conclusions

Putting aside whether we have a housing bubble and whether we have world-beating high house prices, it is clear that housing affordability and general housing market movements have become a critical social and economic issue in this country.

The RBA’s views on some of the economic issues have been discussed above. However, the social issues have also been addressed at times by RBA staff.

Some Observations on the Cost of Housing in Australia, Anthony Richards, Head of Economic Analysis Department, Address to 2008 Economic and Social Outlook Conference, The Melbourne Institute, Melbourne – 27 March 2008

Renters will be worse off when housing prices rise whereas those who own rental property will be better off. Owner-occupiers may be largely unaffected, since they can be thought of as being ‘hedged’ against increases in the cost of housing. There are also generational differences. Younger people who have not yet bought homes will be hurt by higher housing prices. Older owner-occupiers may benefit from an increase in prices if they are intending to extract part of the increased value of their homes. Of course, if older people pass on some of their increased wealth to younger relatives, the gains and losses of these two age groups will be reduced. Indeed, the biggest difference may be between those who benefit from transfers from older relatives and those who do not. Both home ownership and ownership of rental property tend to rise with incomes (Graph 2), so it is lower income households that tend to suffer from rising housing prices and higher income households that tend to gain. But although there are significant distributional effects across the age and income structure, one can make the case that the population in aggregate does not benefit from increases in housing prices.

The most frequently argued point for an imperative to tread lightly on housing policy is indeed just how vulnerable the runup in prices has left our economy. That is ironic in the extreme!

Already the early response to the Royal Commission amongst vested interest is a scare campaign that any consequent tightening of lending standards will lead to reduced access to credit and falling home prices.

This has the effect of suggesting that the error is actually in returning to an economy based on prudent credit availability. That is (convenient) non-sense!

What’s more, one has to wonder just how much of the current “credit crunch” from tightening regulation being discussed is an attempt by the financial sector to reassert its influence over the political bureaucracy.

The real error was, of course, in the permissive allowance, if not encouragement, of the leveraging up of Australian households in the first place!

We are cajoled in an attempt to make us fearful of what may happen if our home prices were not so high. By definition this means that we must, as a consequence of continued high home prices, be accepting that future generations of Australians will need to either take on significantly more financial risk than earlier generations to buy their own home, for even the “fortunate ones” who receive contributions from property-owning parents and other relatives, or accept that they are “have nots” in our society based largely on property wealth which was set in train by the turn of the millennium.

We have moved a long way from the proudly egalitarian society at the end of the previous millennium. However, judging by the way politicians argue around the point of what is fair, they are well aware (from polling and focus groups) that Australians really do cling strongly to those ideals and are craving an inflexion back towards a fairer society.

This is the power and the potential of this Royal Commission, especially if it can break free of the complex headwinds touched on above and the period of inquiry be extended and the TOR expanded.

The issues raised in this submission give rise to very many questions. Perhaps some key questions are these:

- Have our regulators exhibited an asymmetric bias to the risks surrounding our housing markets where their response function is significantly more active to the risks around downside movements in house prices rather than upside movements. In other words, have regulators been slow to react when prices rise, underestimating the risk around rising prices – in relation to duration and rate of the uptrend – thus being slow to react and being cautious to not overly influence the market, while overestimating the risks around falling prices, thus being quick to react to falling prices and being prone to underestimating the strength of policy responses?

- If there has indeed been an asymmetric bias to these risks, is it appropriate and proportional to the actual risks?

- What are the factors that may be consciously and subconsciously affecting regulators when making these decisions?

- Is it the role of regulators to foster “confidence” in the economy?

- If so, what frameworks are being utilised in deciding just how much “confidence” is required?

- And how is the desire to foster “confidence” in the economy balanced with the obligation of senior financial public servants to provide to our society unbiased and trustworthy economic research and opinion of the highest quality?

- Finally, are the regulators doing all they can to play a role in providing information to the public, in an accessible form (easy to understand to the general public), so that our citizens – those who have built the country to what it is today, and those who will make it what is in the future including through taxation and other contributions – can make fully informed decisions and contributions?

While I must admit to being unsure which of these questions can, in effect, be addressed in a Royal Commission, due to a lack of understanding of the legal issues, from a decade of experience in railing for a fairer housing market in Australia, it seems to me that they cannot and will not be addressed anywhere else.

The Royal Commission has done an excellent job thus far at exposing some of the conflicts that have become embedded in the financial services industry through the long period of economic success, much of it based on (almost continuously) upward moving home prices.

Now it is time to go the rest of the way and really pull the rug back to determine just how widespread has been the dulling of senses to the voice of risk, and what are the reasons for this, so that all Australians can work towards a better future for themselves and their families, and for our society collectively, with full confidence that rewards for hard and smart work will be shared fairly.

© Copyright Brett Edgerton 2019

You must be logged in to post a comment.