A 20 year perspective

In my “Open to Offers” post I gave credit to Jeremy Grantham of GMO for much of my understanding of bubbles.

While accurate, absent context this gives a false impression of my own evolution.

The truth is I have always been naturally contrarian. In reality I think all authentic contrarians are that by nature.

I have often pondered on why this is and I consider it, like most character traits, a product of nature and nurture. I have a cautious innate nature mixed with a learned anti-authoritarian streak from my father both as a result of his comments when I was young and as a consequence of major setbacks he suffered which I witnessed (as I have discussed on my ‘About Me‘ page and in other posts on MacroEdgo).

My father’s parents were adults with young children in the Great Depression and his comments to me as a young boy about bank and national finances not being as certain as many assume remained with me.

I understood very early that few people understood risk, or even tried to, so it was wise to approach commonly accepted ‘truths’ and consensus with a degree of scepticism.

I became interested in economics, finance and investing in 1996 when I was 26 as I approached the completion of my PhD. Having become acutely aware of just how much income I had forgone until then to become a research scientist, and understanding the impact of that on my future family with my wife, I had a strong drive to learn as quickly as possible how to use our savings optimally to give us financial security.

I began reading weekend newspapers mainly for business and economics coverage. And soon I began reading books. Even though share market participants were almost unanimously exuberant, the first book I chose to purchase was “How To Handle A Bear Market” by Bill Harper which was published in 1998.

Choosing to read that book at that time was no more by chance than it was for Bill writing it then.

Besides the typical general financial planning books by Paul Clitheroe amongst others, I read Robert Shiller’s “Irrational Exuberance” and did so soon after its release in 2000. Moreover, after reading it I wrote to Robert Shiller from Germany in 2002 when I was there on a Humboldt Fellowship, asking Prof. Shiller for some reprints of his papers.

So even though I have tried to read everything Jeremy had to say over the last decade, I already had a natural interest in learning about speculative manias and bubbles well before I knew of Jeremy or GMO, the funds management firm he co-founded.

I wrote most of the content on the Australian house price bubble on my former blogsite homes4aussies before I began reading Jeremy’s writing, and my commentary at Bubblepedia, at Steve Keen’s blog ‘debtdeflation’, and at many other places, was influenced from my broad reading on speculative manias, though I instantly recognised much of my own viewpoints in Jeremy’s writing (and even his writing in his Latest Viewpoints reminds me of what I was saying back 15 years ago – that ‘analysts’ countering the bubble viewpoint always insist on the identification of a catalyst or pin prick, but that the dynamics of bubbles create conditions so a pop is possible without an obvious catalyst).

Soon after, Jeremy commented on the Australian house price bubble in one of his famous quarterly newsletters which led one member of a (friendship?) group of economists – who gave all appearances of being very protective of the bubble – to attempt to ensnare Jeremy in a wager, which I presumed was to counter the negative publicity around such a highly regarded ‘bubble-spotter’ highlighting it and that being presented to the Australian public through the press.

Another member of this group, who had been described publicly by the above almost as Australian economists’ answer to Crocodile Dundee (pig hunting, rodeo-riding, etc, etc – CRINGE!), had publicly ambushed Steve Keen at a speaking event apparently because he had dared to point to the house price bubble. I listened to a recording of the engagement and it sounded to me like Steve was embarrassed into the wager.

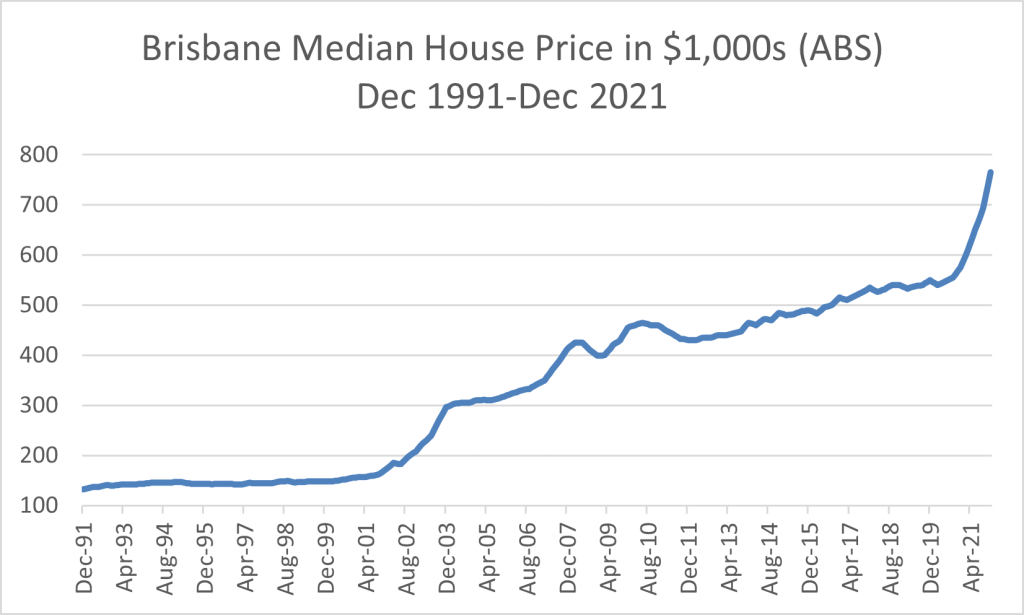

I, myself, tried to establish a wager with someone who gained broad media coverage in releasing ‘research’ which simply applied the recent exponential growth in Brisbane house prices in perpetuity to forecast a $1 Million median price by 2015. Even though that market displayed several more periods of irrational exuberance, in concert with the broader Australian housing market as a result of repeated Government interventions whenever housing markets looked shaky (discussed below), till this day (now double the forecast period) the Brisbane median house price has not gotten nearly that ridiculous to reach that level, although the most recent bout of craziness through the pandemic years was impressive (see graph at end). *

This article about that bet with Steve Keen gives a flavour of the strength of opinions around Australia’s house price bubble, and the prolonged nature of the debate. Note also that the economist who initiated the bet with Steve Keen had a very high profile at the time and was frequently on television, but his public-facing profile fell shortly afterwards and has remained that way over the intervening decade which may or may not be indication of the consequences of behaviour which I, personally, feel fell short of professional within the public eye.

In writing this account I conducted a brief search to learn the extent of my digital footprint from this period and was surprised by how little is available, at least to the broader public. That’s a shame. If the reader ever happens to see the ABC footage of the first day of Steve Keen’s walk from Canberra to Mt. Kosciuszko, after losing that bet, you will see a balloon inflating until it busts with someone’s voice saying “negative gearing… capital gains tax discount… first home owners grant… first home owners boost….” – that’s my voice 🙂

These other bits and pieces should give a fairly clear view of what my activism was then about:

- This article in the Sydney Morning Herald was inspired by my questioning of recently installed Prime Minister Rudd at a community cabinet meeting in northern Brisbane, and was entitled “Rudd Grilled On Housing“. The article at the header of this post was then published in the South East Advertiser on 16 April 2008. What these reports do not capture, though I have stated it online on occasion and in my submission to the banking royal commission, is that at the same meeting the then Treasurer Wayne Swan looked me straight in the eyes and said that I was dreaming if I thought negative gearing would ever be ended. Given my vulnerable state at that time, it literally took every ounce of restraint that I could humanly muster to control my emotions and not react to his arrogant provocation;

- This is a comment on Open Forum in response to an article by Stan Small, an Anglicare outreach co-ordinator who worked with disadvantaged and/or homeless young people, which explains much of my motivation to help the broad community; and

- My submission to the ‘Henry Tax review’.

Still, that Australia’s housing bubble has not yet popped has confounded many of us contrarians, and it really is worthy of discussion. I will share my own thoughts based on 20 years of observing it, partly in hope that it might encourage Jeremy to do likewise.

In my submission to the ‘Henry Tax Review’ I gave a detailed account of the early period of the Australian house price bubble, both in the body of my submission and in the appendices including the paper “Anatomy of Australia’s Housing Bubble” which I wrote in 2008 and which I consider stands as a very good record of what had occurred to that point.

It is fair and accurate to say that in 2007-08 I thought that the chances that Australian house prices would not drop back to more normal levels, i.e. a price to income ratio of near 3x, over the following decade were extremely low.

(In my defence, nobody foresaw such ridiculous central bank shenanigans as the quatitative easing and negative interest rates that we became desensitised to over that period, and which further lifted global debt levels.)

Nonetheless, we did personally buy our one and only family home in 2011 during a lull in the market, not because we thought it was a smart financial decision, but because it was at a period of least financial disadvantage relative to the emotional premium gained from raising our (then young) family in our own home. With over a decade of hindsight we will freely confirm that emotionally we gained everything that we had hoped and probably more.

I do not consider that decision to have been especially financially advantageous, because I still expect that long term price correction, even though financially it has not been as disadvantageous as it could have been – i.e. had the market correction occurred early in our ownership and through misfortune in employment and/or health we became so vulnerable that we needed to sell.

It is equally important to note, however, that even though several specific events/factors have allowed us to pay out our mortgage recently, including the windfall capital gains from positioning for strong falls in the sharemarket as the world was shocked by the challenge posed by the COVID-19 pandemic, these have served to make me realise just how challenging it was to pay out such a large debt with a young family, wanting to provide life-enriching experiences for developing young children, even when we had a very large deposit (40% of the purchase price – almost half of that a windfall from a property sale that was never intended to be an investment), and borrowed significantly less than lenders would have given at the time, for a significantly more modest home than we could have purchased if we borrowed to the max.

In this sharply rising interest rate environment I truly feel for those who were naive and believed lenders when they told them that they had the capacity to pay back mega mortgages and so mortgaged themselves to the max. Our experiences suggest that even people who borrowed a decade ago, irrespective of whether they are well into positive equity, will find it challenging to pay down their debt.

That is the main problem with house price bubbles – the market price of the asset is ephemeral and set based on the transfer of a small proportion of the market, but the debt is constant and is only reduced by paying down principal on top of the interest.

Therein lies another major vulnerability with Australia’s house price bubble. Many small scale Australian property investors don’t pay, and never intended to pay, any of the principal back to the lender. They have been sucked into the market by Government incentives known as negative-gearing (borrowing heavily so that costs including interest and property maintenance outweigh earnings with the deficit claimable as a refund through the personal income tax regime) combined with capital gains tax concessions such that in the bubble many have increased their book wealth by borrowing to the maximum through interest-only loans to buy multiple investment properties.

Look at my submission to the Henry tax review to see an example of how schemes to buy an investment property annually to maintain leverage were spruiked to Australian property speculators who considered themselves investors.

I’ve seen the excitement grow in the eyes of recent arrivals to Australia as I’ve explained these tax perks to them, but the problem is immediately apparent to non-Australians – what happens when prices fall and/or, even worse, stagnate over a prolonged period?

This has become the ultimate weakness of the Australian economy in this new millennium.

The truth is that this serious vulnerability to the Australian economy has long been identified by international investors. In the period after the GFC there was much discussion about the potential for our housing markets to implode taking down our economy and banking sector like the bursting of the US house price bubble. In the face of these persistent questions from the international investment community, which RBA officials and bank executives frequently admitted, the CEO of Australia’s largest bank took it upon himself to do an international roadshow with the aim of soothing these concerns. When the slides of that presentation were released to the public an eagle-eyed contrarian in Australia noticed how the data that were supposed to ‘prove’ that Australian property prices were just high, but not in a bubble, appeared to be cherry-picked in a less than ethical manner to support the claim (i.e. house price data were used inconsistently which had the effect of lowering price to income multiples).

The intended takeaway from that presentation, which was dutifully reported in the Australian press, was that although Australia indeed had very high house prices relative to income by both global and historical standards, the supply of new housing was constrained such that demand for its actual utility – as shelter – continually outstripped it, and since that situation appeared intractable, it could not be a bubble because the price would never strongly correct downwards.

If I was an intelligent analyst at those presentations I would also have reflected on the concentration of banking in Australia, noting that the small number of major lenders to house buyers were also major sources of funding to developers.

In other words, the businesses and their self-interested executives that have the most to lose from the house price bubble popping have had an enormous level of control over all of the supply and demand levers of relevance, as long as the supply of capital remained unconstrained. Even then the RBA used the cover of the GFC to provide funding to the banks and it was only with that period distant in the rear view mirror that the public was informed about near collapses amongst our smaller banks that had been rapidly growing market share selling mortgages.

What about the regulators, you say….

Well I think the abundant systematic biases which create enormous asymmetry – and disadvantage – in Australian housing markets are well inferred to this point, but if we fast forward and concentrate on the period from 2017 until now a very clear picture of it emerges.

An interesting year in the Australian housing market was 2017 because one member of our quartet of heads of financial bureaucracies (which together make up the Council of Financial Regulators) actually admitted that we had a bubble in housing markets, and another essentially admitted it in all but name.

“I have been saying for a while that I thought it was a bubble and other people are catching up now,” was what Greg Medcraft, head of the Australian Securities and Investment Commission, said.

Wayne Buyers, head of the Australian Prudential Regulation Authority, clearly had similar concerns when he was asked whether he thought it was a bubble and responded, “I don’t use the B word. I refuse to use the B word. It is superficial.“

Clearly these very senior bureaucrats had become spooked by the sheer level of irrationality in the exuberance that had been reached surrounding our housing markets for a decade and half.

APRA then enforced tighter lending standards especially on interest-only loans which some fretted might – in itself – cause a ‘US-style meltdown’. Capital city housing markets weakened. Mortgage stress also rose and commanded attention.

Let’s recall, then, that 2018 was the year of the Royal Commission into Misconduct in the Banking, Insurance and Financial Services Industry. The public push for a banking royal commission was prolonged but resisted by the political class until ex-investment banker Prime Minister Malcolm Turnbull was left with no alternative but to give the go ahead in December 2017.

The banking royal commission ran through 2018 and the banks finished up the year on the ropes.

My own submission centred on expanding the Terms of Reference to look at the roles of the financial regulators in perpetuating the housing bubble and especially the RBA, mainly discussing events that happened under the leadership of Glenn Stevens.

The year was literally full of the most shocking revelations – just when you thought you had heard the worst possible ways in which people would mistreat others on behalf of organisations, another even worse revelation was unearthed. Truthfully I don’t want to be reminded of them by searching, so I would suggest the reader google “banking royal commission” for the period 2018 if they wish to be ‘sold’.

For me the real low point, however, was the pompous testimony of the National Australia Bank Chairman Ken Henry, who had left his post as head of the Australian Treasury early in the decade as one of Australia’s most highly regarded economic bureaucrats. Both he and CEO Andrew Thorburn resigned their lucrative banking executive positions in February 2019 as a direct consequence of revelations and their perceived lack of contrition displayed when testifying.

All through 2019 there was much discussion of which of the royal commission’s 76 recommendations would be enacted.

It seemed that, finally, the stranglehold that the banking industry had over the political system in Australia was utterly broken, and along with it the preferential place that property speculation had in our economy. It seemed that the housing bubble could no longer be perpetuated by vested interests.

It is accurate and fair to say that, given the sheer shock and outrage at the bankers, most in the public expected significant actions to be taken.

The banks and their lobbyist clearly had a different viewpoint, unsurprisingly.

In May 2019 the failure to elect a new Labor Prime Minister, in Bill Shorten, who had struggled with personal popularity, but who ran strongly on clamping down on inequities which favoured those with asset wealth, by dismantling negative gearing and other tax advantages, showed that those in the financial services industry could still influence political outcomes.

Then, less than a year later, the first fast-moving global pandemic in a century provided distraction so that the public lost focus on the issue altogether. As we all know, nothing much else at all mattered more than whether we were entering or exiting lockdowns, and what was the current situation for mask mandates.

By January 2021 less than half of the recommendations of the Royal Commission had been enacted. Worse still, in September 2020 the Morrison Government sort to loosen responsible lending laws by removing the obligation on the lender to check the capacity of the borrower to repay the debt.

Of course, the instruments of political interference in markets go beyond those made explicit in policies, laws and other official documents.

When the pandemic began to bear down on our economy, it was hardly any surprise that the first thing the Morrison Government sort to do was stimulate the housing market, as had been the economic ‘playbook’ in Australia for the past 2 decades of the bubble. The HomeBuilder grant was spawned and announced to the public on 4 June 2020.

The curious thing for me was that already by August, a family member who is in the building industry – a co-owner of surveying businesses that had been in business for over 25 years – was telling me that June 2020 was a record month for them, that was until it was beaten by July, which was on course to be bettered by August! And they did not know what do with the piles of money they were given for the JobKeeper program (though their accountant thought it a good idea to keep it in the bank for the moment, just in case they were asked to pay it back!)

The point is that it was clear to me that such a rapid activation was not by accident or chance, and it would seem highly likely to me that bankers were told (by Government representatives) to shovel money out the door without fear of reprisal for how exactly they did it!

Now we have even more heavily indebted young households that are extremely vulnerable with interest rates rising, still heavily indebted less young households that have planned for continual price appreciation to numb the sensation of standing in debt quicksand increasingly stressed, older Australians who have realised that there is more to life than working into old age to accumulate even more housing ‘wealth’ after their own mortality was highlighted in the pandemic, and we have several generations of Australians tired of being told they should go without ‘luxuries’, such as smashed avocado, to enter a lifetime of debt servitude and financial vulnerability to buy a home while being afraid that they will not have a home to rent because $billions given to ‘investors’ over decades has failed to deliver sufficient supply of new homes… because it was never meant to!

So what are the lessons here?

For me it is very simple. No matter what we are told, the answers to this apparently intractable problem have always been easy to determine in big, empty Australia (the words of Sir David Attenborough – see here in “The Conundrum Humanity Faces But Nobody Admits“).

The problem is the politics amongst our elites who have grown fat on power for the sake of self-interested influence rather than doing good, or even leading.

The general public must also share blame because enough have allowed themselves to become deluded that they have become wealthy, far more than genuinely are, while others have become fearful that their poor financial decisions will haunt them, such that many are willingly complicit in the increasing entrenchment of a two-tiered society of owners and vulnerable renters.

But why has the bubble not popped?

Because what happened in the US forewarned the elites that our even larger housing bubble needed to be managed as an utmost priority at all times.

Thus successive Governments and economic bureaucrats, not wanting it to pop on their watch, became stewards of a house price bubble not a national economy. That is why genuine economic reform has been off the table for over 2 decades!

The US economic bureaucrats were (almost comically, if not for the harm done to everyday Americans) blissfully unaware of the risks that had been allowed to build in their housing markets and broader economy before it popped in 2006.

On the other hand, RBA Governor at the turn of the millennium, Ian Macfarlane, has on occasion indulged himself with a congratulatory lap of honour for taming an early period of irrational exuberance in our house price bubble in 2002/03, which in that 2020 interview he put down to “something that was really harmful, which was pure speculative activity, particularly through negatively geared acquisition of second, third, fourth, fifth properties [so much so that] it was starting to get pretty crazy then and it was starting to get pretty close to a bubble.“

It has been clear since this period that confidence at the RBA runs high at being able to repeat such ‘feats’.

I guess they now have some reason for that confidence, but I do wonder whether it really is something of which to be proud. Moreover, I do wonder whether the ‘Tin Tin’ that emailed me at homes4aussies all of those years ago with a research paper empirically proving the extent of distortion in housing markets caused by negative gearing and capital gains tax concessions would be satisfied with what has occurred over the intervening period. For those who do not know, the little known nickname of the current RBA Governor Phillip Lowe is ‘Rin Tin Tin’, and to be clear, yes, from the moment I read a biography on him when he assumed the position of Governor, I have believed it was he that emailed me.

The really interesting thing is this. The debate the RBA was involved with 20 years ago, and by the way, which ‘Tin Tin’ wrote on during his time at the Bank For International Settlements, if I recall correctly, is whether a bubble can be leant on to prevent damage to an economy when it busts.

What the RBA has proven is that a bubble can be perpetuated a very long time. In doing so, I would suggest that as much damage to the economy and society has been done, perhaps even more.

Will the price of Australian houses ever be around 3x earnings again, the commonly accepted level for affordability?

Yes!

When?

When will we have a prolonged period of quality political leadership? Okay, I did answer with a question, but if you know the answer to that one, let me know.

The current Government looks good, but with so much work to be done, will they be able to progress a full program without losing electoral favour – just out of the whims of a general public that struggles to hold its attention on much any more – and how high up the order of priority will fair housing policy be placed?

Sometimes I do wonder whether the Whitlam strategy is not better, even if it takes 50 years for the broad public to catch up with what an enormous achievement it was to heave the nation through major roadblocks.

Then again, if we get really bad bubble managers and/or a confluence of difficult to manage factors, which might just prove to be the current situation, more the latter than former, then the once in a generation bust that would ensue will wring out the exuberance for generations such that homes will cease to be valued as casino chips and will be priced again based on their utility… probably around 3x annual earnings.

*For those inclined to be sympathetic to the realestate agents’ ‘optimistic’ forecasting, and might point out that my own forecast made at a similar time (that I published within my Tax submission – to hold myself accountable, I might add) proved to be too ‘pessimistic’, I will point out the Australian Bureau of Statistics measure for the median priced Brisbane house was $483,500 in the March quarter of 2016. So my forecast was 30.9% less than the actual, whereas the realestate agents’ forecast was more than 100% above the actual median price! The wager that I had proposed was for $20,000 to the winner (him if median price was over $1million, me if less) and $10,000 for each complete $100,000 over/under as the case might be. I was, however, prepared to negotiate and use the average of our respective forecasts at $667,000, though with some modifications of amounts and increments. If the realestate agent accepted the challenge I probably would have used the wager as a ‘hedge’ and gone ahead and bought then. Finally, remember who got the publicity of having their forecast published in national newspaper, whereas the editor of the paper that I contacted to help establish the wager was not at all interested in the story… lest they promote someone providing an alternative view to the bubble spruikers.

Postscript: I leave the reader with a graphical representation of all of this – a graph of the Brisbane median house price over the total time that I have observed it… This picture tells a million or more words, not a thousand… The ABS series was ceased after the December 2021 release… nice to end it on a bubble high… in a once in a century global pandemic!

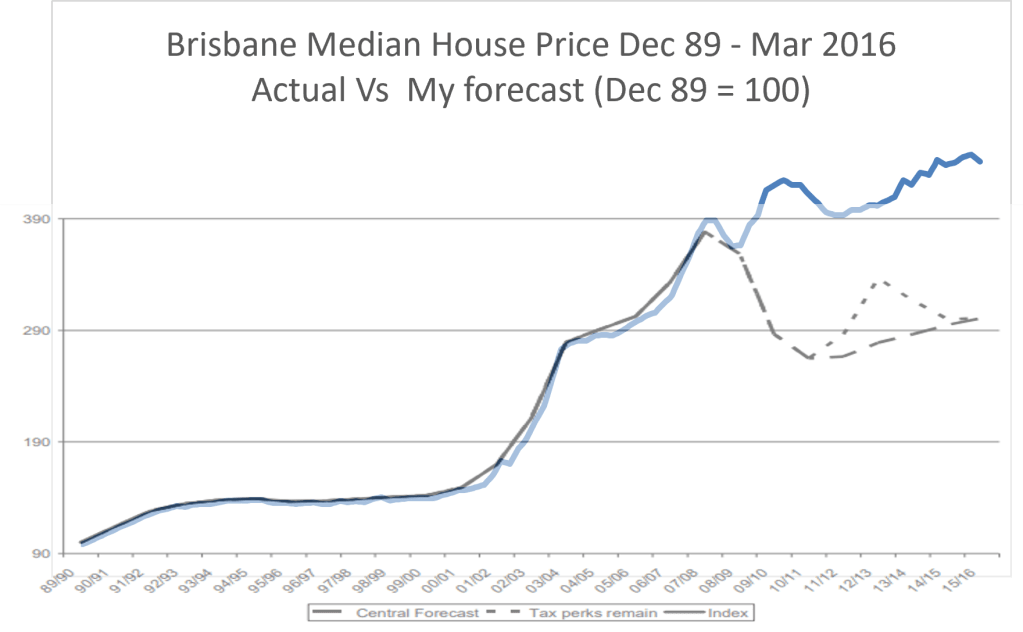

Finally, just for fun, here is my forecast (as available in my submission to the Henry tax review, available for download above) overlayed over a graph of actual, with the ‘actual’ part of my forecast (solid black line) aligned so scaling is correct…

Edit: Two paragraphs dealing with when I began reading Jeremy’s newsletter were edited significantly within a few hours of posting because a reader, clearly familiar with my work, viewed the file below which showed that I began reading Jeremy’s newsletter in late 2008 (I believe it was likely the newsletter of his that I discussed in the paper that led me to become a regular reader).

Gained value from these words and ideas? Consider supporting my work at GoFundMe

© Copyright Brett Edgerton 2023

One thought on “[RESET]> The ‘Great’ Australian House Price Bubble”

Comments are closed.