I can easily imagine how confused must be the typical Australian household.

At the beginning of last week we were told in a private data release that in November 2019 house prices across the nation increased at their quickest rate in 16 years

By the end of the week we were told how weak was our economy. National accounts had shown that our economy grew at the slowest rate since the depths of the Global Financial Crisis, and that we were in a “private recession” which was only prevented from being an actual recession by increased Government spending.

We were then told that the consumer has gone missing even though the Government had pumped dollars directly into bank accounts.

Unfortunately the Australian public can not turn to the Public Servants that head our Reserve Bank who should be the bastion of wisdom and most able to shine a light on what is the actual situation. No, as I have pointed out here and here these boffins seem to have cosied up to their political masters and business elites to be cheerleaders and peddlers of that all too elusive emotion loosely defined as “confidence”.

The contradictions are truly staggering and one wonders what would be the expression on the face of Ian Macfarlane if one was to jump through a wormhole and make reference to these (current) conditions in a press conference hosted by the then RBA Governor circa 2006:

- House prices surging at 1.7% per month, the fastest in 16 years and at 2.7% per month in Sydney (on a simple annual basis, of multiplying the monthly rate by 12, of 32.4%) and prices in Melbourne and Sydney – 50% of the national housing stock by value – within a few percent of record high nominal prices,

- unemployment 5.3%,

- Immigration of 1.7%,

- Historically high resources prices, and

- Low Government debt compared with other comparable nations.

Counterbalanced against:

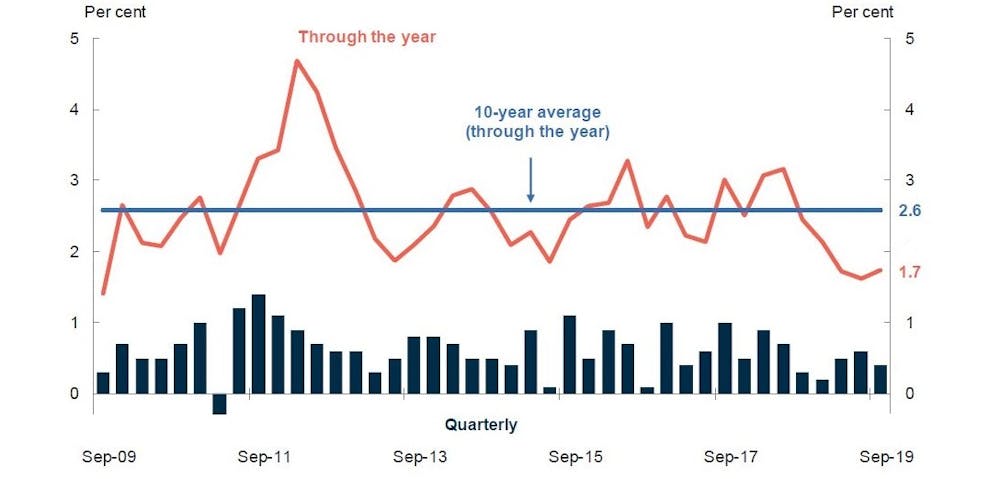

- an inflation rate (consumer prices index) persistently below the 2-3% band,

- a RBA overnight cash rate at 0.75% having halved over the last 6 months,

- the majority of the nations’ economists forecasting another 2 cuts of totalling 50 basis points during the next year, and

- a RBA having publicly discussed experimental or non-conventional monetary policy known as quantitative easing as the potential next step, which Governor Macfarlane back in 2006 most likely would have immediately identified as “money printing”, and which most of those same national economists expect the RBA will commence soon after the RBA reaches the 25 basis point cash rate lower bound.

It seems clear to me that Governor Lowe, who now has Ian Macfarlane’s former job, succeeding Glenn Stevens in between, is simply trying to put some blinkers on the consumer for one last hurrah, to the benefit of a long struggling retail sector in the hope that there will not be a further wave of closures in the post-Christmas lull.

At this stage it appears that Australians are not falling for the spin and collectively households have decided to recognise the elephant in the room – our debt which is now threatening to breach 200% of household income, and most certainly will do so if the runup in house prices broadens into greater transaction numbers which would be expected as prices approach record levels.

This is the conundrum to which I have long pointed. In order to keep our house prices elevated the majority of buyers will need to borrow significant sums – relative to the asset price and especially to their income – and with an absence of wage growth (for all of the reasons I detailed here and here) this is making the credit ratios of most individuals, and certainly of Australian households in aggregate, deteriorate.

Oh how quickly we move in contemporary politics and thus policy. Does anybody remember this discussion from all of 18 months ago when APRA was considering imposing limits on loan to income ratios for banks when lending for home purchases? The limit being discussed was 6 to 1, and when the ratio of median house price to median household income is around 9 to 1 in Sydney and Melbourne it was hardly surprising that many felt implementation would seriously curtail the market.

Another titbit that I recalled when reading back on my earlier comment was how at around that same time ex-RBA board member, Prof Warrick McKibbin, was suggesting that the level of household debt and house prices was not of concern and suggested that if the RBA wanted it should stress test the situation by increasing interest rates. In my comment I suggested that this was probably what the RBA and the other members of the Council of Financial Regulators had in mind in driving through price increases on interest free mortgages.

So how did that episode work out? I would suggest that there were more than a few stresses exhibited.

But that is now history. An abrupt turnaround in prices has been manufactured by halving the cash rate to 75 basis points and by, instead of stiffening macroprudential policies further, easing up on them.

This truly is the definition of a bubble and is an essentially unsolvable problem.

As I discussed here (at Investment Theme Debt Monetisation), the November 2019 RBA chartpack showed that house prices fell sharply during the period that those housing credit ratios stabilised. Now that prices are rising again those credit ratios will get worse as sales increase.

The RBA now admits that they misunderstood the impacts of falling house prices on consumption. No doubt they are hoping that rising house prices will have a positive impact. However, not all that long before this mea culpa they were arguing that falling prices would not result in a negative wealth effect because the earlier period of rising prices was not associated with a positive wealth effect.

So why would we have a positive wealth effect from rising prices now?

The larger bubbles blow the less stable they become and the more volatile the price movements. Essentially if prices are not increasing strongly then they are likely to fall sharply.

We have been disappointed by a procession of leaders and treasurers, both intentional lower case. Remember how Joe Hockey realised in his final speech in parliament that negative gearing was not good for the country, and Wayne Swan, as the President of Federal ALP, has in fact decided that it is not a dream but a necessity to end negative gearing (see here for his comments directly to me when he was treasurer).

Though entirely unsatisfactory, we must realise that from the perspective of a lower case leader they are incentivised to delay the inevitable as much as possible even if the consequent bust will be worse. After all, politicians are no more incentivised to do the right thing by the electorate other than if it aids in victory at the next election.

Alternatively, if they delay the reckoning – or kick the can – enough such that the depths of the downturn are not felt until the following Government is in power then they can obfuscate and shift maximum blame on their political opponents.

Any close observer of the Australian housing bubble knows well that there is plenty of blame to be shared by both of our major political parties.

Unfortunately for the Australian people, all of this means that being stuck with a sclerotic economy for a very prolonged period is perhaps the best outcome that can be contemplated. The more rapid path of dealing with the debt overhang is perhaps the worst recession that Australia will suffer since the Great Depression.

Which path we follow is not especially manageable and we remain extremely vulnerable to external shocks, and the more household debt we take on, the more that vulnerability grows. It is for this reason that the credit ratings agencies continue their pressure on the Federal Government to be prudent fiscal managers even in a world where many major economies are conducting non-traditional monetary policy.

In an email that I send to friends in May 2018, and which I posted online almost a year ago, I predicted that Australia would be in the grips of a serious downturn by now. I suggested that the high rate of immigration and resources exports might prevent the actual definition of a recession being met, but that the downturn is likely to turn out to be severe.

The temporary boost to confidence from the surprise re-election of the Morrison Government and their greater incentive to kick the can has slowed the pace of decline. But for all of the reasons that I detailed above, all that has been achieved thus far is a delay which has only served to increase the imbalances.

Meanwhile, more Australians are waking up to the poor quality of Australian leadership, and that is only underlined more as we observe a smoke-haze blood red sunset over Sydney and Brisbane.

Soon nobody will buy what the confidence sellers offer no matter what discounts they spruik…

Gained value from these words and ideas? Consider supporting my work at GoFundMe

© Copyright Brett Edgerton 2019